INFO

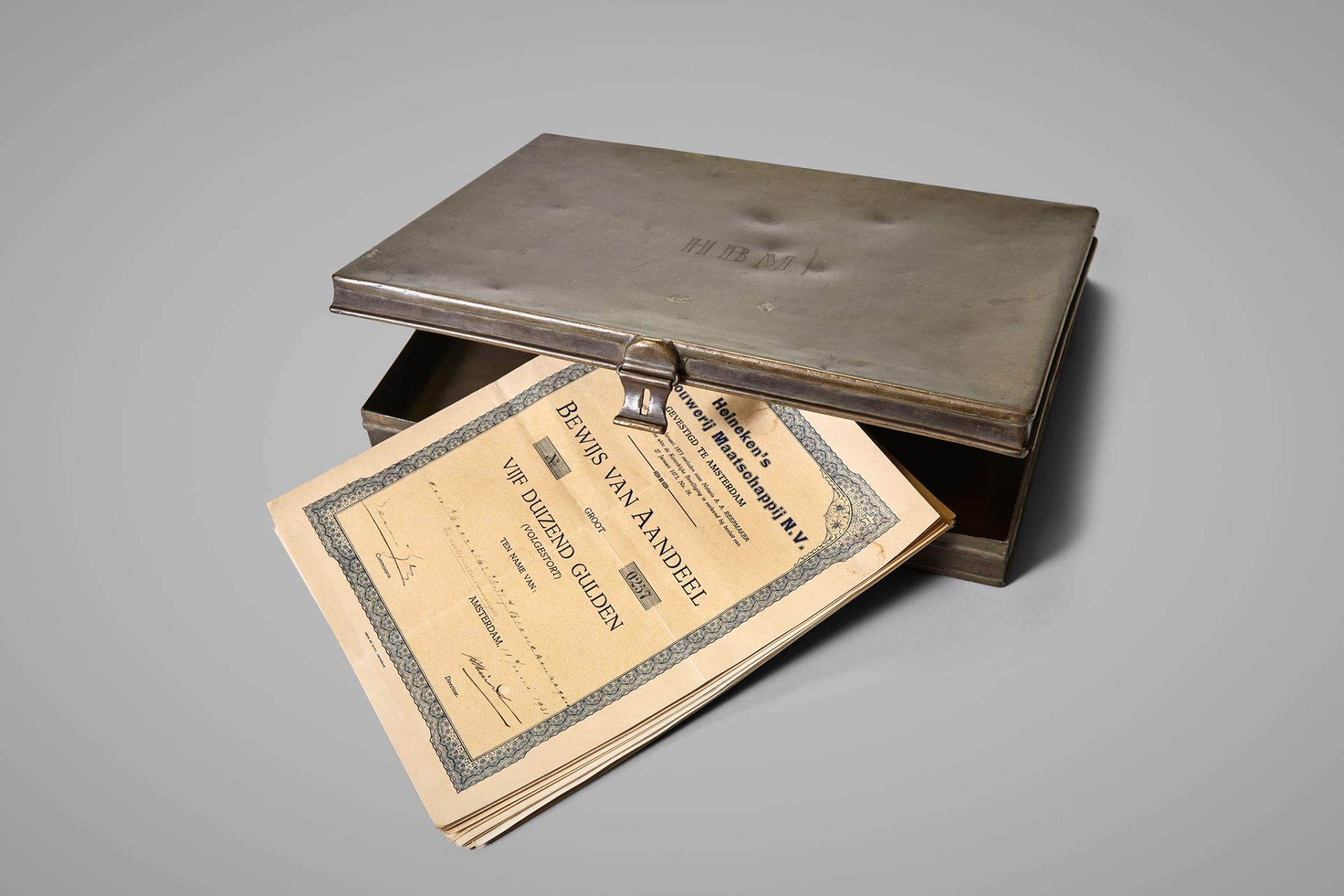

Metal box with shares of Heineken's Beer Brewery Company

1931

metal, paper

h 4.4 x w 27.5 x d 36 cm

Shareholders are persistent

With the declaration ‘All or nothing,’ the company’s founder laid the ground for Heineken's corporate history in 1864. In that year, Gerard Adriaan Heineken acquired the shares of 80 investors in De Hooiberg Brewery. Barely a decade later, in 1873, Gerard Heineken established the public limited company Heineken's Beer Brewery Company (HBM).

However, in this joint venture with Willem Baartz and Hubertus Hoyer, owners of the Rotterdam d'Oranjeboom Brewery, Heineken couldn't be the sole shareholder. A total of 40 investors contributed 1.2 million guilders, divided into 240 shares. This was a substantial amount at the time, especially considering that Heineken had paid only one-fourteenth of that value for De Hooiberg.

Cautious approach

From the outset, the company’s financial strategy was cautious. Despite the success of Bavarian beer and its export, Gerard Heineken invested the profits largely in research and development. The dividends, shared profits for the shareholders, as well as the tantièmes, payments to the management and board of directors, were modest. When Gerard's son Henry became the CEO of HBM in 1917, he maintained this conservative approach toward shareholders: dividends stayed relatively low. However, reserves increased significantly; development was financed to the extent possible from retained earnings. The tantièmes, on the other hand, grew substantially in the following years.

Crisis – but not at HBM

In the 1920s, the world faced increasingly challenging economic conditions. While HBM's board members and accountants urged sharing more profits with shareholders, the management maintained its conservative dividend policy. In 1924-1925, less profit was allocated to the reserve fund, only to reach unprecedented heights thereafter. However, the management and board members hardly reduced their own remuneration. In 1929, as the New York stock market crash ushered in the years of the Great Depression, their tantièmes were higher than ever before. An interesting note: Mary Petersen-Tindal, a major shareholder and Henry's mother, expressed a preference for distributing a higher amount to the management and board members rather than sharing the profits with shareholders.

Discontent

Shareholders began voicing their discontent. So much so that in 1930, HBM decided to allocate an additional 1.2 million guilders and issue extra shares to mollify them. The matter was thus resolved without major repercussions. However, the situation changed after Mary's death two years later and the appointment of Dirk Stikker as the new CEO in 1935. Under Stikker's leadership, HBM prepared for a renewal of its financial policy and the skewed capital structure, particularly due to the impending introduction of a new tax law that might compel HBM to share the entire profit with shareholders.

Fiscal manoeuvre

A recapitalisation took place in 1938, raising the share capital from 2.4 to 12 million guilders. Heineken's Beer Brewery Company became publicly listed. Existing shareholders were more than satisfied, receiving four new shares for every old share surrendered. Through this clever fiscal exchange manoeuvre, they also avoided paying taxes on the generous dividend payout on the old shares – after all, they no longer owned them. HBM's stock market debut in 1939, an issuance of 2,500 shares each valued at 1,000 guilders, conclusively ended the debate over profit sharing. The rest is history.